If you’re selling into the consumer products space, chances are good that you are dealing with the very cumbersome issue of deductions. Deductions, also known as chargebacks or short payments, impact the entire business cycle including manufacturing, distribution, finance and even human resources. While these transactions individually may not pose a huge financial risk, the frequency of occurrence and high-volume nature creates an efficiency burden on the business that requires attention, leading to increased costs spent on enough staff to address the manual nature of deduction management. While finance assumes the burden of managing these challenges, the impact on the total customer experience is an indicator of product quality, performance and overall satisfaction.

Challenges Faced by All

Deductions create an interesting dilemma for consumer products companies. As most mass market retailers short pay the majority of all their invoices, reconciling and resolving these transactions can often times be a laborious process requiring man hours and labor investment. Yet 85 to 90 percent of deductions are valid, with corresponding credits sitting on an account or waiting for internal approvals. With only a 10 to 25 percent chance of finding invalid claims, the burden becomes sifting through hundreds, sometimes thousands, of transactions to find the few that can be returned to the customer with a demand for payment—that is, if the retailer’s rules allow for claims to be returned individually. Many retailers require quarterly settlement events in which the negotiation of payment often results in 50, 40, even 30 percent of the original amount due. All this leads to a huge cost burden with a minimal return and is a driver for letting these transactions age without resolution.

Aged deductions create an even more pervasive problem. As a deduction ages, financial reporting becomes less reliable. Days sales outstanding (DSO), a common receivables performance measurement, is calculated using the total receivable as one variable. Normally, DSO increases as invoices age, a sign that the receivable is not performing well and the length of time needed to obtain payment greatly exceeds the customer’s payment terms. With a deduction-heavy portfolio, aged deductions have the same impact as aged invoices, with one major caveat. The total receivable value is inflated by accounts receivable (AR) that simply isn’t collectible (remember 85 to 90 percent result in a credit or adjustment). A reported DSO of 95 days may, in actuality, be more like 55 to 65 days once the valid deductions are scrubbed from the books.

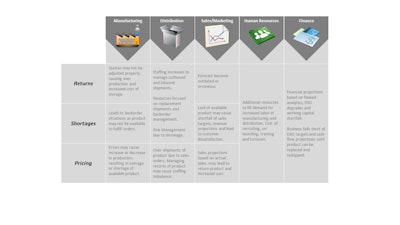

Leaving deductions unmanaged or slowly managed also weakens internal sales forecasting. As the sales and marketing department reviews sales statistics by customer, it may not be taking into consideration the volume of product that a customer may be returning, thus creating a circular imbalance from production to human resources. Using the table above, we can see how each type of deduction impacts each of the core business functions:

It’s clear from the above that unmanaged deductions impact the entire business. Just two or three months of inefficient or negligible attention to these transactions could throw the entire organization into confusion, and leads to an unnecessary cost burden, performance shortfalls and, for public companies, less than favorable financial reporting to the street.

Getting Your Arms around the Problem

While managing this process seems like an insurmountable task, there are various ways to institute controls and methods, taking a marriage of people, process and business analytics to achieve success. In some cases, management believes that, if it hires some additional temporary labor, it can help reduce the problem. While adding staff is certainly an option, adding staff that is not fluent in the retailer practices may not fix the problem and could lead to even bigger issues. Retailers frequently reopen periods for claims audits, testing the validity of the reconciliations and, more worrisome, the claims that were previously settled.

While every retailer takes some form of deduction off their invoices, each one operates under a different set of rules and requirements. A good first step in managing the problem is identifying a tolerance you are willing to offer the customer. Perhaps every deduction under $25 is automatically adjusted without review, bringing down the manageable volume. While effective in reducing manual touch points on small transactions, a sampling should be pulled bi-annually to ensure customers aren’t taking advantage of the instituted tolerance levels.

Identifying how each customer deducts and creating workflows for each deduction type sets a baseline for customer behavior management. The key term here is behavior management. This payment pattern, in its complexity and volume, is specific to mass market retailers. Expecting Wal-Mart to change its behavior is a fruitless battle, so accepting this fact and learning to control the process as efficiently as possible is the only solution. An investment of resources and time to conduct customer-specific whiteboard sessions is a good first step. The customer receivables team should have good insight into these processes.

Technology solutions are the final piece of the deduction management puzzle. Integrating third-party bolt-on tools is a good workaround, as most businesses aren’t going to perform a new enterprise resource planning (ERP) implementation to combat this issue and many companies struggle with information technology (IT) resources to perform tasks timely. These delays lead to aging transactions and the challenges explained above.

Partnering with a vendor that already has this expertise could greatly increase the chances of success. Qualified vendors already have access to the talent needed to deliver high-quality performance and a catalog of best practices for managing mass market retailers. Both of these factors mitigate the risk associated with potentially inexperienced staff, high turnover and the initial time investment spent establishing baseline processes. They should also have the tools and technology in place to manage the volume of deductions. Automated cash application tools and specialty applications for managing deductions makes them more efficient, resulting in greater accuracy and reduced time to resolution. Having access to their own IT resources that are dedicated to designing these solutions also takes the labor burden off of internal IT resources. Bringing together the three major components of managing this challenge is a must-have operating model.

There Is Hope

The only true industry standard is that all mass market retailers take deductions from their invoice payments. With the large volume of transactions hitting the books every month, managing the problem casually only leads to flawed business data, over- or under-stocked inventory, and a cost burden that’s felt through the entire business. Everyone from human resources to marketing and sales to IT are impacted by the burden of managing this process. By implementing some of the solutions discussed, sound processes, analytics and business acumen drive improvement, increase control and help your CFO sleep better at night.