Many large and global organizations are setting ambitious goals related to sustainability. Along with public commitments to human rights and more ethical forms of procurement, these organizations are also making big promises to reduce or completely neutralize their greenhouse gas (GHG) emissions.

Through recent research, however, APQC found that many organizations may be completely or partially in the dark about a significant source of emissions: their logistics providers.

Organizations Can’t Go it Alone On Sustainability

As organizations face increasing pressure to leverage more sustainable supply chains, it makes sense that they would want to start pushing for greater sustainability within their four walls. For example, moving to paperless processes, buying energy from renewable sources, and eliminating Styrofoam cups from the breakroom are all choices that can help to reduce an organization’s carbon footprint.

The challenge is that Scope 1 and Scope 2 emissions—that is, emissions from company facilities and those generated by an organization’s utilities providers—only account for a small part of an organization’s overall GHG emissions. Scope 3 emissions, which include logistics providers and any other indirect upstream and downstream emissions not included in Scope 2, account for 80% and in some cases as much as 90%+ of an organization’s overall emissions. This means that organizations that are serious about sustainability cannot go it alone—they need to collaborate with logistics providers (and other Scope 3 partners), achieve full visibility into their practices, and regularly disclose Scope 3 emissions data to identify opportunities for reducing emissions.

APQC finds that too many organizations are missing critical opportunities to achieve greater transparency with their logistics providers. Supply chain transparency has two relevant parts. Visibility—accurately identifying and collecting data from all links in your supply chain—and disclosure—communicating that information, both internally and externally, at the level of detail required or desired. Both parts are necessary for organizations to better screen their logistics providers against criteria for environmental sustainability.

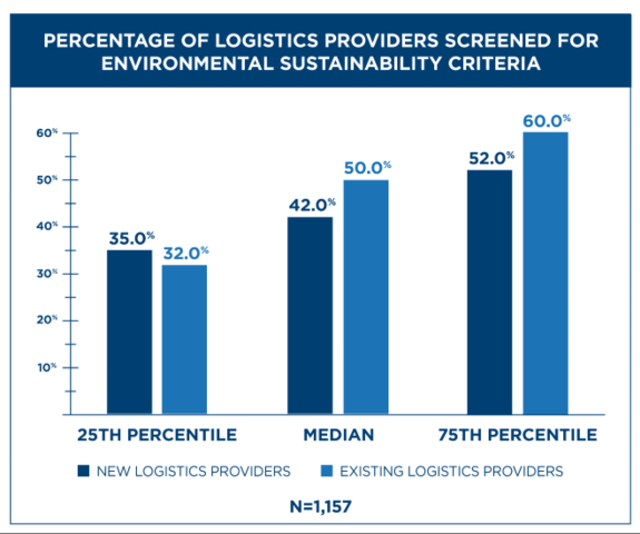

APQC has found that organizations at the 25th percentile only screen around a third of their new or existing logistics providers against sustainability criteria. Even organizations that do more screening (those in the 75th percentile) only screen around half of new logistics providers and 60 percent of existing providers (Figure 1).

Figure 1APQC

Figure 1APQC

These percentages are much lower than we would have expected. Given what we know about the impact of Scope 3 emissions, these organizations are likely missing a big and very important piece of the puzzle in their sustainability efforts.

Why screening Logistics Providers’ Sustainability Matters

Organizations that don’t assess all of their logistics providers’ environmental sustainability practices and results could be opening themselves up to unnecessary risk, especially as laws and regulations governing sustainability become more stringent. Yesterday’s “nice to have” forms of sustainability reporting are quickly giving way to mandatory laws and regulations. These changes are happening in countries across the globe. In the U.S., for example, in March 2022 the SEC issued Release No. 33-11042, the Enhancement and Standardization of Climate-Related Disclosures for Investors. Assuming this rule goes into effect in its current form, it would require an SEC registrant to disclose its Scope 3 emissions if that information is deemed material to understanding an organization’s business. The Departments of Energy, Transportation, Housing and Urban Development and the Environmental Protection Agency are also collaborating on a National Blueprint for Transportation Decarbonization that is sure to add additional pressure on logistics providers and the companies that contract with them.

Even in the absence of laws and compliance requirements, groups of investors like the Net Zero Asset Managers initiative, The Paris Aligned Investment Initiative, and the Net Zero Asset Owner Alliance are transitioning their investment portfolios toward net zero GHG emissions by 2050 or sooner. Organizations that only track half of their logistics providers will increasingly be left behind in favor of those that collaborate with all of their logistics providers and prioritize sustainability across their entire value chain. And those organizations making promises that they cannot keep (or report against in a credible manner) will be tried in the court of public opinion by consumers—which is often more damaging than the fines and penalties imposed by the legal system.

Key Takeaways

Organizations are facing pressure from multiple sources to ensure that their supply chains are operating in a sustainable manner from end-to-end. Organizations that do not currently track and assess the sustainability of their logistics providers may be left scrambling when Scope 3 disclosure requirements are no longer optional but instead become mandatory. Additionally, with anti-greenwashing laws becoming a reality, the need for this provider data as evidence of sustainability will continue to increase.

More broadly, organizations with publicly stated commitments to environmental sustainability should be prepared to demonstrate that they are actively working with their logistics providers to reduce GHG emissions. This is not possible if these organizations only screen 50% (or fewer) of their logistics providers against these criteria. End-to-end supply chain transparency is rapidly becoming a business necessity, requiring organizations to evaluate critical environmental practices of new and existing logistics providers.