New York — December 18, 2008 — When considering the global trade environment in 2009 there are a number of potential issues looming that can disrupt global supply chains, sourcing strategies and the flow of working capital. Several issues are hangovers from 2008's economic turbulence and some are just starting to develop. If not properly addressed, importers and exporters may face significant unexpected costs and increased disruptions to their supply chain.

But the news for 2009 isn't all bad. A number of promising opportunities exist as well. Below are nine trends that will continue to challenge multinational businesses for at least the next 12 months.

Supply Chain Risk Mitigation in an Economic Downturn

In times of economic downturn, leading companies will focus on restructuring supply chain operations to better position themselves to grab additional market share and profits as economies around the world start down the path of recovery. A large part of supply chain re-engineering efforts focus on driving out inefficiencies while balancing risk. Supply chain risk mitigation will receive increased focus this coming year versus past downturns due to many factors:

- Supplier financial risk. As financial weakness permeates the marketplace, we already are seeing a rise in supplier bankruptcies. Companies will need to re-evaluate their supply chains to identify and support their key partners and reduce the number of potential "weak link" suppliers. At the same time, multiple suppliers for a single product or part must be secured to ensure supply chains keep running. Expect more dual or multi-source procurement of raw materials, parts, subcomponents and assemblies to counter supplier financial risk, to develop sources closer to end-markets, and to hedge currency swings and future inflationary pressures in different regions and economies.

- Volatility in energy, commodity, labor rates and currency exchange. Companies need to factor into their decisions potential fluctuations in future energy and commodity prices, as well as labor and currency exchange rates. Some industry sectors, such as industrial goods and construction, are likely to see robust price increases as major economies around the world announce economic stimulus packages focusing on major infrastructure programs. Any resulting boom could produce another run of sharp increases in some commodities and energy.

- Unpredictable economic recoveries. Economic recoveries will likely be unpredictable and somewhat choppy across regions. The ability to quickly react to global shifts in demand will be critical for success. More redundant manufacturing capability should be established across multiple geographies in order to realize better time-to-market for end customers and to be able to balance and buffer demand globally. Redundant manufacturing also can serve as a hedge against currency swings and future inflationary pressures in different economies.

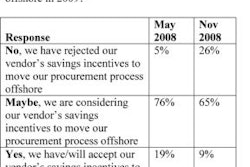

Searching for Working Capital

As traditional sources of capital — such as bank lending — dry up or become more expensive, companies will look for alternative sourcing of working capital — and looking at internal operations is a logical direction. This trend will bring increased scrutiny to the supply chain as companies look to reduce inventory and lower operating or carrying costs.

In addition, buyers will look to extend payment terms, while suppliers will drive to collect receivables more quickly, creating the need for a liquidity buffer — such as supply chain financing — to mitigate this brewing payables/receivables conflict. The current credit environment is pushing buyer/supplier partnerships to look to their trade flows to drive the creation of additional liquidity.

A Resurgence in Letters of Credit

The recent downturn in global markets is expected to reduce demand for commodities and associated goods and services from recent peaks, but the reduction in available credit for trade financing has been much sharper.

J.P. Morgan, the largest issuer of letters of credit in the United States, has seen resurgence in the use of letters of credit to facilitate the financing of international trade. In these uncertain times, letters of credit are a traditional, secure way of doing business and of financing the underlying trade between buyers and suppliers. The increase in letters of credit usage became noticeable toward the end of 2007 as surpluses of working capital for open account financing began to dry up.

Recently, fewer banks have been willing to extend and guarantee credit, so the supply has been declining, and in some cases, the cost has risen dramatically. For the right borrower and the right transaction there are still deals to be done, but the market will remain tight for the near future.

Shortening the Supply Chain

J.P. Morgan continues to see U.S. manufacturers reconfiguring their supply chains by moving plant operations and sourcing vendors closer to home and away from Asia. Limited free trade agreements, high energy costs, and rising labor and production costs in Asia all contribute to companies reevaluating extended supply chains.

While opportunities still exist in Asia, Mexico has become an increasingly popular source for manufactured goods as companies compete on time-to-market strategies, seek financial advantages found in Mexico's multiple free trade agreements, and capitalize on Mexico's investment incentives, streamlined customs processes and abundant English-speaking workforce. The U.S. Department of Commerce reports a 7.2 percent increase from year-to-date imports through Mexico compared to the year before.

Mexican customs officials have been piloting a new customs regime that seeks to attract more foreign investment by improving importers' supply chain speed and mitigating the delays frequently associated with time-intensive processes and procedures at the port of entry. A customs regime is a country's specific set of trade regulations, processes and practices that regulate the actions of importers and exporters. The government believes that this new customs regime, known as Regimen de Recinto Fiscalizado Estratégico (RFE), will decrease logistics cost in terms of dollars per container and numbers of days in transit which, in turn, will help attract additional production to Mexico.

The program is expected to open for additional manufacturers in early 2009. Mexico Customs estimates that the new clearance process will save an importer between US$200 and US$600 per shipment.

Other highlights: goods can remain in a Mexican warehouse for up to two years on a tax-free and duty-free basis; the elimination of customs inspection at the port of entry, resulting in cost reductions and reduced time-to-market; no secondary customs inspections required; a simplified customs clearance process resulting in reduced Customs Brokers fees; and a three-day grace period for importers within which to correct import declarations.

More Free Trade Agreements and More Scrutiny

More than 200 bilateral and multilateral Free Trade Agreements (FTAs) exist around the world today. In 2009, more growth and duty savings opportunities will arise for manufacturers, but with a new administration soon in power in the United States, will FTAs continue to prosper?

The United States is expected to finalize three new FTAs in 2009 with Colombia, Panama and South Korea. Whether or not the existing FTAs on the table will be a priority for the new U.S. administration, many companies still risk leaving millions of dollars worth of duty savings unclaimed with the FTAs already in force.

In addition, U.S. Customs and Border Protection is expected to increase scrutiny of FTA claims and the ability of importers to substantiate their claims. The complexity associated with understanding and leveraging FTAs is beyond the scope of many companies because they either lack the expertise, resources, technology, or all of the above to do it efficiently and cost-effectively. Many companies eventually come to a decision point: either invest internally or outsource to a global trade expert.

China Clamps Down on Oversight

The embarrassing toy and milk product recalls that triggered unexpected supply chain costs and negative public attention for multinational manufacturers has also attracted the attention of Chinese officials who fear the mass pull-out of foreign businesses. Chinese officials have vowed to clamp down on product safety failures by launching national investigations and ordering local officials to report all possible product safety issues. The regulatory environment is expected to become stricter in China with the introduction of a control list or catalogue of commercial encryption products developed and made overseas.

Impacting hi-tech manufacturers outside of China, this new control list calls for tighter regulatory oversight of firms that use encryption technology within their products. Encryption technology is used to protect information within many military, government and civilian systems, such as computers, networks, mobile telephones, wireless microphones, wireless intercom systems, Bluetooth devices, and bank automatic teller machines. The Beijing-based State Encryption Management Commission intends to release the list in 2009. All foreign-based firms importing CEPs into China will need to create detailed processes and procedures for China CEP license management.

New Import Challenges — The Amended Lacey Act

The United States is now the first country in the world to prohibit the import, export, sale or trade in illegally harvested wood and wood products. An amendment to the 108-year old Lacey Act will require detailed reporting (scientific name, quantity, value and country) of any plant matter incorporated into an imported product brought into the United States.

This law broadly covers plants used in processing, no matter how miniscule the amount and no matter how far removed from the harvesting of the plant. The amendment could have significant consequences for U.S. importers who will be subject to new data reporting requirements. The specific scope of what items are covered under the amendment is still being defined, with Congress acting to reduce the burden on trade. For example, plant matter used in the creation of shipping labels and manuals may not have to be reported. The first phase of enforcement is expected to begin in April 2009.

Violations of the Lacey Act provisions are expected to be prosecuted through either civil or criminal enforcement actions.

A Global Eye Toward Consumer Product Safety

In August, the United States signed into law the Consumer Product Safety Improvement Act (CPSIA), presenting certain manufacturers and importers with a new set of regulations to manage. Considered to be the most sweeping consumer product safety law enacted in decades, the new law is expected to usher in similar regulation around the world to addresses safety standards and requirements for children's products, such as mandatory testing, the reduction in the use of lead paint, and more visible cautionary statements related to choking hazards.

In November, representatives from China, the European Union and the United States met in Brussels for the first high-level trilateral summit on product safety to discuss key developments and further joint activities to improve cooperation and the exchange of information relating to consumer product safety. Upon import, products must be accompanied by certification that they comply with all applicable consumer product safety rules and similar rules, bans, standards and regulations under any other laws administered by the importing nation.

About the Author: As the Global Product Executive for the Logistics product suite with the Global Trade Services group at J.P. Morgan, Bernie Hart leads a business of 650+ employees that delivers end-to-end global risk management and operational solutions. www.jpmorgan.com/trade