Digitalization is clearly a driver for industrials mergers & acquisitions (M&A) growth, as industrial companies are targeting acquisitions in technology, communications, and media. A few recent examples: Toyota Motor Corp bought a $1 billion stake in the ride-hailing firm Grab. Broadcom acquired CA Technologies to strengthen its position in software and cloud technology. General Dynamics acquired CSRA Inc.—a provider of high-tech IT solutions—for approximately $9.7 billion.

Being close to the customer is an increasingly important success factor for industrials companies, as reflected by these 2018 transactions:

● Schneider Electric purchased industrial software company Aveva to strengthen full life-cycle solutions for its customers.

● Cisco acquired Duo Security to provide secure connection solutions.

● Siemens bought Mendix to facilitate app development for its Industry 4.0 platform MindSphere.

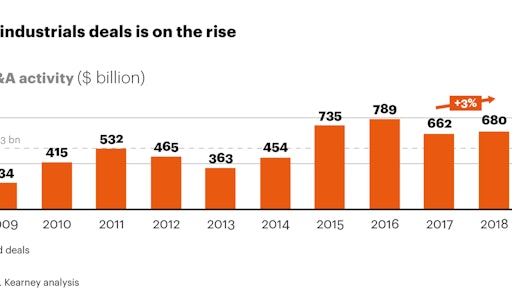

2018 saw more than 100 deals worth over $1 billion, including seven transactions that topped the $10 billion mark. In one noteworthy megadeal, United Technologies acquired Rockwell Collins for more than $32 billion.

Consolidation within sectors drove much of the industrials M&A activity in 2018. For example, Northrop Grumman strengthened its space business with the acquisition of Orbital ATK, while Safran and Zodiac merged to form a top-three supplier for the aircraft industry.

2019 M&A Outlook

Our recent survey of leading industrial firms, investment banks, and investors suggests this is only the beginning of a global wave of deals to build industrial value chains. In North America, 65 percent of respondents anticipate that industrials M&A deal volume will grow by 10 percent or more this year. The corresponding figures for survey respondents from Western Europe, China, India, and were 57 percent, 53 percent and 56 percent, respectively.

As shown in Figure 2, these informed observers expect technology access and consolidation will be the top drivers of industrials M&A growth in 2019.

The anticipated rise in technology access plays seems particularly noteworthy. In fact, it feels past due.

While growth is the darling of most investors, traditional industrials are often perceived to have low growth potential, and so are regularly subject to low valuations. By making sound, high-profile technology acquisitions, industrials companies can quickly gain some of the high-tech patina that investors associate with fast growth.

Of course, the quest to secure tech access is driven by much more than hopes for an immediate boost in share price. Everyone can see that digitization will reshape the future of industrials across both the manufacturing and product side. In automotive, for example, electric propulsion and autonomous driving increasingly look like transformational forces. Overall, the imminent reality of The Fourth Industrial Revolution has a growing number of manufacturers scrambling to make ready for the digital future.

For these reasons and more, technology access is arguably now the most important key to getting the portfolio right in industrials—an assertion clearly supported by the 2019 M&A outlook.

CFO Imperatives

This certainly merits the attention of CFOs, who are among those most explicitly accountable for ensuring the company is well positioned for sustained profitable growth. Specifically, CFOs should:

Foster a sense of urgency. The 2019 M&A outlook strongly suggests that the best technology targets may be gobbled up fast. CFOs need to emphasize to the CEO and board that if they do not move early on prime targets, their first, second or even third choice might soon be gone.

Make certain the balance sheet is ready to act on opportunities. Do not let the financials be the reason the company misses out on a strategically essential acquisition or investment.

Balance tech investments and deal structure. The company can build, buy or borrow (i.e., via joint ventures/license deals) the new capabilities and technologies so essential to driving future growth. The CFO provides a crucial perspective on which path may be best, and on what kind of deals should bring the greatest growth and earnings potential to the firm.

Securing technology access will largely determine the fate of many if not most industrials companies. The time to act is now. And the CFO has a vital role to play in charting a successful course through what promises to be a momentous year in industrials M&A.